Square Merchant Account: 2026 Review

If you want to start accepting credit cards as a merchant in 2026, Square is one of the most popular choices for a variety of reasons. This merchant services provider has fairly transparent credit card processing fees, supports a variety of industries, and offers decent protection for merchants.

However, Square’s payment processing is far from ideal, and there are plenty of cases where alternative solutions could help you maintain a better cash flow.

Here’s everything you wanted to know about Square for payment processing in 2026.

Get approved for a high-risk merchant account in less than 24 hours

What is Square? Key features

Square is a payment processing platform that allows businesses to accept credit cards, debit cards, mobile wallets, and online payments through a single system. It combines payment processing, point of sale software, hardware devices, and basic business management tools.

The platform is known for its simple setup and flat rate pricing. Small businesses can start accepting payments almost immediately using a mobile card reader, a POS app, or an online checkout page.

Square is popular with small retailers, restaurants, service providers, and freelancers who want an easy way to process payments without negotiating merchant account contracts or complicated pricing structures.

These are the most important features you should know about.

POS system for in-person payments

Square is best known for its point of sale system, which allows businesses to accept payments in physical locations.

The Square POS app runs on tablets and smartphones and works with Square’s hardware devices such as card readers, contactless terminals, and full countertop registers. Businesses can process payments using chip cards, tap to pay, magnetic stripe cards, and mobile wallets like Apple Pay or Google Pay.

The POS software also includes tools for product catalogs, inventory tracking, receipts, refunds, and sales reports.

For many small businesses, this POS setup replaces a traditional cash register. You can even accept payments using your phone if you don’t wish to buy any additional hardware to accept payments.

Online payments and ecommerce tools

Square also supports online payments through its ecommerce and checkout tools.

Businesses can create a simple online store, add payment buttons to a website, or send payment links directly to customers through email or text. Square integrates with many website builders and ecommerce platforms, making it possible to accept online payments without building a custom checkout system.

Payments made online are processed through the same Square virtual terminal used for in-person transactions.

Payment links and invoices

With Square Invoices, businesses can generate invoices and send them to customers by email or share a payment link that opens a hosted checkout page. Customers can then pay using credit cards, debit cards, or digital wallets.

This is handy for service businesses such as consultants, contractors, and agencies that need to bill clients after completing work.

Square hardware ecosystem

Square offers a full range of payment hardware that connects directly to its software platform.

Examples include mobile card readers that plug into a smartphone, wireless contactless terminals, and complete POS registers with built-in receipt printers and customer displays.

Because the hardware is designed specifically for Square’s system, setup is usually straightforward and requires little technical configuration.

Business management tools

Beyond payment processing, Square includes several basic tools for running a business.

These include inventory management, customer directories, employee time tracking, reporting dashboards, and appointment scheduling for service businesses.

Many of these tools are included in the standard Square account, while more advanced features require paid add-ons or industry-specific versions of the platform.

Integrations with other business software

Square connects with a wide range of external software tools.

Businesses can integrate Square with:

- accounting platforms

- ecommerce systems

- CRM tools

- marketing software

- restaurant management systems

- and many other tools

These integrations allow payment data to flow between systems for reporting, bookkeeping, and customer management.

For companies that want a single ecosystem to handle payments and business operations, this integration layer is one of Square’s biggest advantages.

PS. we also have a comparison between Square and Stripe that you may want to read.

Is Square really a merchant account provider?

Square allows you to accept credit cards and process payments, which makes it look like a traditional merchant account provider. In reality, Square operates as a payment service provider (PSP) with an aggregate merchant account rather than a dedicated merchant account provider.

That difference has important implications for fees, account stability, and approval requirements.

Square uses a shared merchant account model

When you sign up for Square, you are not issued an individual merchant account with an acquiring bank. Instead, your business processes payments through Square’s master merchant account before they reach your bank account.

This means Square groups thousands of businesses together under the same merchant processing infrastructure.

For small businesses, this approach has some advantages:

- Quick approval with minimal paperwork

- No underwriting process before you start processing

- Simple flat rate pricing

- Fast onboarding

You can usually start accepting payments within minutes of creating an account.

However, the shared account model also means Square has much stricter automated risk controls.

Why Square freezes or closes accounts

Because Square processes payments for many businesses under one merchant account structure, it monitors transactions very aggressively.

If the system detects activity that looks risky, the platform can automatically:

- Freeze payouts

- Place funds on hold

- Request additional documentation

- Suspend or terminate the account

This can happen even if a business is legitimate, especially if the system detects:

- Higher than expected sales volume

- Large transactions

- Sudden spikes in processing activity

- Higher refund or dispute rates

Unlike traditional merchant accounts, these decisions are often handled by automated risk systems rather than a dedicated account manager.

Traditional merchant accounts work differently

A true merchant account provider works directly with an acquiring bank to create a dedicated merchant account specifically for your business.

Before approval, the processor performs underwriting to evaluate risk factors such as:

- Industry type

- Business model

- Average transaction size

- Chargeback risk

- Processing history

While the approval process takes longer, it usually results in:

- Higher processing limits

- Greater account stability

- Fewer sudden freezes

- Support from an account manager

This model is important for high-risk merchants that process larger transactions or operate in industries with elevated chargeback rates.

What this means for high-risk businesses

Square is designed primarily for low-risk businesses with predictable sales patterns, such as retail stores, coffee shops, and small service providers.

Businesses in higher-risk categories often run into problems because Square’s policies prohibit or heavily restrict many industries.

Companies that sell high-ticket products, subscription services, or operate in regulated industries may find their accounts limited or closed once processing begins.

In these cases, working with a specialized high-risk merchant account provider that supports high-risk businesses is usually a safer option.

Square pricing in 2026

Square uses a flat rate pricing model, which means businesses pay a fixed percentage plus a small per-transaction fee depending on how the payment is accepted. There are no setup fees, PCI compliance fees, or long-term contracts, and the basic POS software can be used for free.

This pricing structure is simple and predictable, without hidden fees, which is one of the main reasons Square became popular with small businesses. However, the flat rate model can become expensive for companies with higher sales volumes or large transaction sizes.

Below is a breakdown of the most important Square fees businesses should know before signing up.

In-person credit card processing fees

For payments where the customer taps, inserts, or swipes their card at a terminal, Square charges:

- 2.6% + $0.15 per transaction

This rate applies to most in-person payments processed through the Square POS app, Square Terminal, Square Register, or mobile card readers.

The same rate applies regardless of card type, so a premium rewards credit card costs the same as a basic debit card.

Online payment fees

For ecommerce payments, checkout pages, and payment links, Square charges a higher rate because the card is not physically present.

Typical online card payments cost:

- 3.3% + $0.30 per transaction on the free plan

Some paid Square plans reduce this to 2.9% + $0.30, depending on the subscription tier.

These fees apply to payments processed through Square Online stores, ecommerce integrations, and hosted checkout pages.

Manually keyed transactions

If a business manually enters a card number into the POS system or processes a stored card on file, Square charges an even higher rate due to the increased fraud risk.

The standard fee is:

- 3.5% + $0.15 per transaction

This applies when taking payments over the phone, entering card numbers manually, or charging a saved card.

Invoice payments

Square Invoices allow businesses to send payment requests to customers through email or a payment link.

Fees depend on how the customer pays:

- 3.3% + $0.30 for card payments through invoices

- 1% per transaction for ACH bank transfers, with a minimum fee of $1

ACH transfers are significantly cheaper than card payments, which is why many service businesses encourage bank transfers for large invoices.

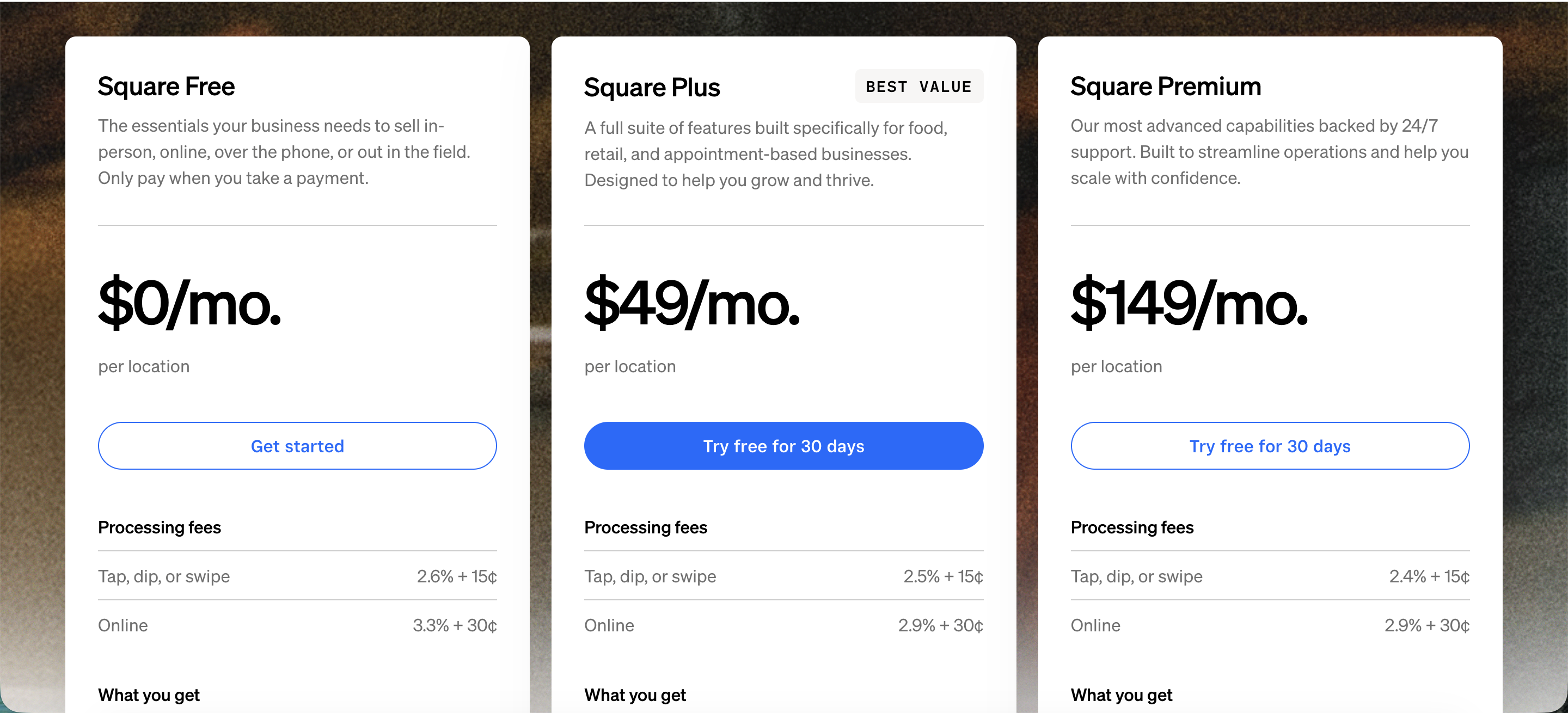

Square subscription plans

While Square offers a free plan for basic POS functionality, businesses can also upgrade to paid subscriptions with lower processing rates and additional features.

Common plans include:

Free plan

- $0 monthly fee

- Standard transaction rates such as 2.6% + $0.15 for in-person payments

Plus plan

- Around $49 per month per location

- Lower in-person processing rates, such as 2.5% + $0.15

Premium plan

- Around $149 per month per location

- In-person fees drop to roughly 2.4% + $0.15

Large businesses that process more than about $250,000 per year may be able to negotiate custom pricing with Square.

Hardware costs

Square hardware is optional but often required for in-person payments.

Typical hardware includes:

- Square Reader for mobile payments

- Square Terminal for countertop checkout

- Square Register for full POS setups

Prices vary depending on the device, although basic readers typically start around a few dozen dollars, while full registers can cost several hundred dollars.

What Square does not charge as a merchant services provider

One of Square’s selling points is that it eliminates many of the traditional payment processing fees.

Square does not charge for:

- Account setup

- PCI compliance support

- Chargeback management

- POS software downloads

- Account inactivity

This simplified structure is attractive to many small businesses, but the trade-off is that the transaction percentages are often higher than traditional merchant accounts, especially for businesses with larger sales volumes.

High-risk industries that Square doesn’t support

While Square is easy to sign up for, it does not accept every type of business. The platform has a long list of prohibited and restricted industries, most of which fall into the high-risk category.

These restrictions exist because payment processors must follow card network rules, banking regulations, and fraud prevention policies. If an industry historically has higher chargebacks, regulatory risk, or fraud rates, Square often chooses not to support it.

For businesses operating in these industries, Square will usually reject the application or shut down the account once the activity is detected.

There are some industries that Square may generally work with, but under very strict limitations. For example, Square’s CBD processing accounts are safe until they suddenly get shut down.

Below are some of the most common industries that Square does not support.

Adult products and adult entertainment

Adult businesses are one of the most frequently rejected categories by mainstream payment processors.

This includes businesses selling:

- Adult content or subscription sites

- Escort services

- Sexually oriented products or services

These industries often face stricter legal requirements and higher dispute rates, which is why many mainstream processors avoid them.

Firearms, weapons, and related accessories

Square generally restricts businesses involved in the sale of firearms and related equipment.

Examples include:

- Firearms and gun parts

- Ammunition

- Certain weapon accessories

These products are highly regulated and present compliance risks for payment processors.

Telemarketing and direct marketing businesses

Many telemarketing and direct response sales models are not allowed on Square.

This category often includes:

- Inbound or outbound telemarketing services

- Infomercial-based sales funnels

- Certain direct marketing offers or subscription funnels

These business models historically produce higher chargeback rates and fraud complaints.

Credit repair and financial services

Several financial services businesses are restricted or prohibited on Square.

Examples include:

- Credit repair services

- Debt collection agencies

- Identity theft protection services

- Certain loan or investment services

These businesses are highly regulated and often classified as high risk by payment providers.

Pharmacies and online medication sales

Square also restricts many healthcare related ecommerce activities.

This includes:

- Online pharmacies that operate without in-person prescriptions

- Pharmacy referral services

- Certain telemedicine medication fulfillment models

Strict pharmaceutical regulations and fraud concerns make these businesses difficult to support on mainstream payment platforms.

Multi-level marketing and affiliate-driven offers

Certain sales structures are also prohibited or heavily restricted.

Examples include:

- Unauthorized multi-level marketing businesses

- Rebate-based programs

- Upsell-driven sales funnels

These models often create billing disputes and refund requests, which increases payment risk.

Illegal or regulated products

Any product or service that violates laws or card network rules is automatically prohibited.

Examples include:

- Counterfeit goods

- Drug paraphernalia

- Illegal products or services

Payment processors must block these activities to comply with financial regulations and card network policies.

Should you get a Square merchant account or not?

Square works extremely well for low-risk merchants with predictable sales, but it can create problems for companies that process higher volumes, operate in regulated industries, or experience large transaction spikes.

Here is a quick way to decide whether Square makes sense for your business.

Get a Square merchant account if

- You run a small retail store, restaurant, or service business with predictable sales

- You want to start accepting payments quickly without a long underwriting process

- You prefer simple flat rate pricing instead of complicated interchange-based pricing

- You need a built-in POS system, inventory tools, and basic business management features

- You process relatively small transactions and moderate monthly volumes

- You want an all-in-one platform for in-person payments, invoices, and simple ecommerce

Don’t get a Square account for payment processing if

- Your business operates in a high-risk industry, such as adult, firearms, travel, or credit repair

- You process large transactions or high monthly payment volumes

- Your sales fluctuate significantly from month to month

- Your business relies on subscription billing or pre-orders with long fulfillment periods

- You want lower processing fees through negotiated merchant account pricing

- You cannot afford sudden account holds or payout delays

Because Square operates as a payment service provider that groups many businesses under a shared merchant account, it uses automated risk systems that may freeze funds or restrict accounts when transaction patterns change, or chargebacks increase.

For companies operating in higher-risk industries or processing larger volumes, a dedicated merchant account provider is often a safer option since it offers more stable processing relationships and higher transaction limits.

Accept payments for your high-risk business with TailoredPay

Square can be a great option for small, low-risk businesses that want a quick and simple way to start accepting payments. For everyone else, Square gives you more limitations than benefits.

Many industries are restricted, and companies that process large transactions, high monthly volumes, or subscription-based payments may experience account holds, payout delays, or sudden shutdowns.

This is where a specialized high-risk payment provider becomes important.

TailoredPay works with businesses that traditional platforms often reject. Instead of using a shared merchant account model, TailoredPay connects companies with acquiring banks that support higher-risk industries and more complex business models.

With TailoredPay, you get:

- Dedicated merchant accounts instead of shared payment infrastructure

- Support for many high-risk industries that Square does not allow

- Higher processing limits and larger transaction support

- Chargeback management tools and risk guidance

- Multiple banking relationships for more stable payment processing

If your business operates in a restricted industry or has struggled with payment processor limitations, working with a specialized provider can make a major difference in long term stability.

Get approved in less than 24 hours