What is an Aggregate Merchant Account and How Does it Work?

Getting approved to accept online payments sounds simple, until it is not.

Many businesses sign up with a payment processor, enter their details, and start accepting credit cards within minutes. Others get declined without a clear explanation, or worse, get approved and then see their funds frozen weeks later.

The difference often comes down to the type of merchant account behind the scenes.

Aggregate merchant accounts have made credit card processing faster and more accessible than ever. They power some of the most popular checkout experiences online and allow small businesses to launch quickly without opening their own merchant account. But they are not built for every business model.

In this guide, we will explain exactly what an aggregate merchant account is, how payment aggregation works, how it compares to a dedicated setup, and what to do if your business does not qualify. Whether you are just starting out or looking for a more stable long-term payment solution, understanding the structure behind your online payments is critical.

Get approved for a merchant account in less than 24 hours

Key takeaways

-

Aggregate merchant accounts allow multiple businesses to process payments under a single master merchant account, making credit card processing fast and accessible.

-

They are ideal for low-risk, small-volume businesses that want quick approval and simple flat-rate pricing without opening their own merchant account.

-

In this model, you operate as a sub-merchant, and the payment processor controls underwriting, compliance, and risk management.

-

The tradeoff is reduced control, including the risk of fund freezes, rolling reserves, or sudden account termination.

-

A dedicated merchant account provides your own merchant ID, full underwriting upfront, and greater long-term stability, especially for high-volume or high-risk businesses.

-

As processing volume grows, interchange-plus pricing in a dedicated setup can be more cost-effective than flat-rate processing fees.

-

If you are declined by a payment aggregator, working with a high-risk specialist like TailoredPay can help secure a stable payment solution for ongoing online payments.

What is an aggregate merchant account, and how does it work?

An aggregate merchant account, sometimes called a shared merchant account, is a type of payment processing setup where multiple businesses operate under a single master merchant account owned by a payment provider.

Instead of getting your own dedicated merchant account with a unique merchant identification number, you are grouped together with other merchants. The payment service provider handles merchant underwriting, compliance, fraud monitoring, and settlement under its umbrella account.

You see this model most often with large payment platforms like Stripe, Square, and PayPal.

How it works step by step

Here is what happens when a customer makes a purchase through an aggregate account:

- Customer enters card details on your website, checkout page, or payment link.

- The payment provider processes the transaction under its master merchant account.

- The acquiring bank approves or declines the transaction.

- Approved funds are deposited into the provider’s master account.

- The provider then transfers your portion of the funds to your business bank account, usually within one to three business days.

From the card networks’ perspective, the payment is processed by the provider, not by your individual business. You are essentially a sub-merchant within that larger account structure.

Why providers use the aggregate model

Aggregate accounts are built for speed and scale. Because the provider is taking on the primary risk relationship with the acquiring bank, they can:

- Approve merchants quickly, often within minutes

- Offer simple, flat-rate pricing

- Handle PCI compliance and fraud tools at the platform level

- Onboard thousands of small businesses without full underwriting upfront

This makes aggregate accounts very attractive for startups, e-commerce brands, and low-risk businesses that want to accept credit card payments immediately.

The trade-off

The convenience comes with a trade-off.

Since you do not have your own dedicated merchant account, the provider has broad authority to:

- Freeze funds

- Place rolling reserves

- Terminate your account

- Hold payouts during reviews

If your chargeback ratio increases or your business model falls outside their acceptable use policy, your account can be suspended with little warning. Because you are pooled with other merchants, risk is managed aggressively to protect the master account.

For low-risk merchants, this structure can work well. For high-risk businesses or merchants with higher-ticket sizes and greater chargeback exposure, a dedicated merchant account is usually a safer and more stable option.

Dedicated merchant account vs. aggregate merchant account

Before we go deeper, here is a side-by-side comparison of the two models.

| Aggregate merchant account | Dedicated merchant account | |

|---|---|---|

| Account structure | Shared master account owned by provider | Unique merchant account under your business name |

| Underwriting | Minimal upfront review | Full underwriting and risk assessment |

| Approval time | Minutes to a few hours | A few days to a few weeks |

| Risk ownership | Provider controls the master account | Direct relationship with the acquiring bank |

| Account stability | Higher risk of sudden freezes | Greater long-term stability |

| Pricing model | Flat rate pricing | Interchange plus or custom pricing |

| Best for | Low risk, small or new businesses | High-risk, high-volume, or established businesses |

Now let’s break down what these differences mean in practice.

Account structure and control

With an aggregate account, you are a sub-merchant under the provider’s master account. Platforms such as Stripe, Square, and PayPal operate this way. You do not receive your own merchant identification number. Instead, transactions are processed under the provider’s umbrella.

With a dedicated merchant account, your business has its own merchant ID and a direct relationship with an acquiring bank. You are not pooled with other merchants. This separation gives you more control and reduces the chance that another merchant’s behavior affects your account.

Underwriting and approval

Aggregate providers rely on simplified onboarding.

Many businesses can start accepting payments within minutes, with deeper reviews happening later. This is convenient, but it also means accounts are closely monitored after activation.

Dedicated merchant accounts require full underwriting before approval. This includes reviewing your business model, processing history, chargeback ratios, financials, and credit profile. The process takes longer, but once approved, you typically benefit from more predictable account treatment.

Risk management and fund holds

In an aggregate model, the provider carries primary risk with the acquiring bank. If your transaction patterns change, chargebacks increase, or your industry is flagged as high risk, the provider can freeze or hold funds quickly to protect its master account.

With a dedicated merchant account, risk is evaluated upfront. While reserves and monitoring still exist, decisions are usually based on your individual performance, not pooled risk. This is especially important for high-risk industries where sudden freezes can disrupt cash flow.

Pricing differences

Aggregate accounts often use flat rate pricing. It is simple and transparent, but it can become expensive as your volume grows.

Dedicated accounts typically use interchange plus or custom pricing structures. For larger merchants, this often results in lower effective rates and more flexibility, especially when negotiating terms such as rolling reserves.

Which one makes sense?

If you run a low-risk business with small ticket sizes and want to start processing payments immediately, an aggregate account can be a practical choice.

If you operate in a high-risk industry, process large volumes, or cannot afford sudden fund holds, a dedicated merchant account is usually the safer long-term solution. For high-risk merchants in particular, stability and clear underwriting matter far more than instant approval.

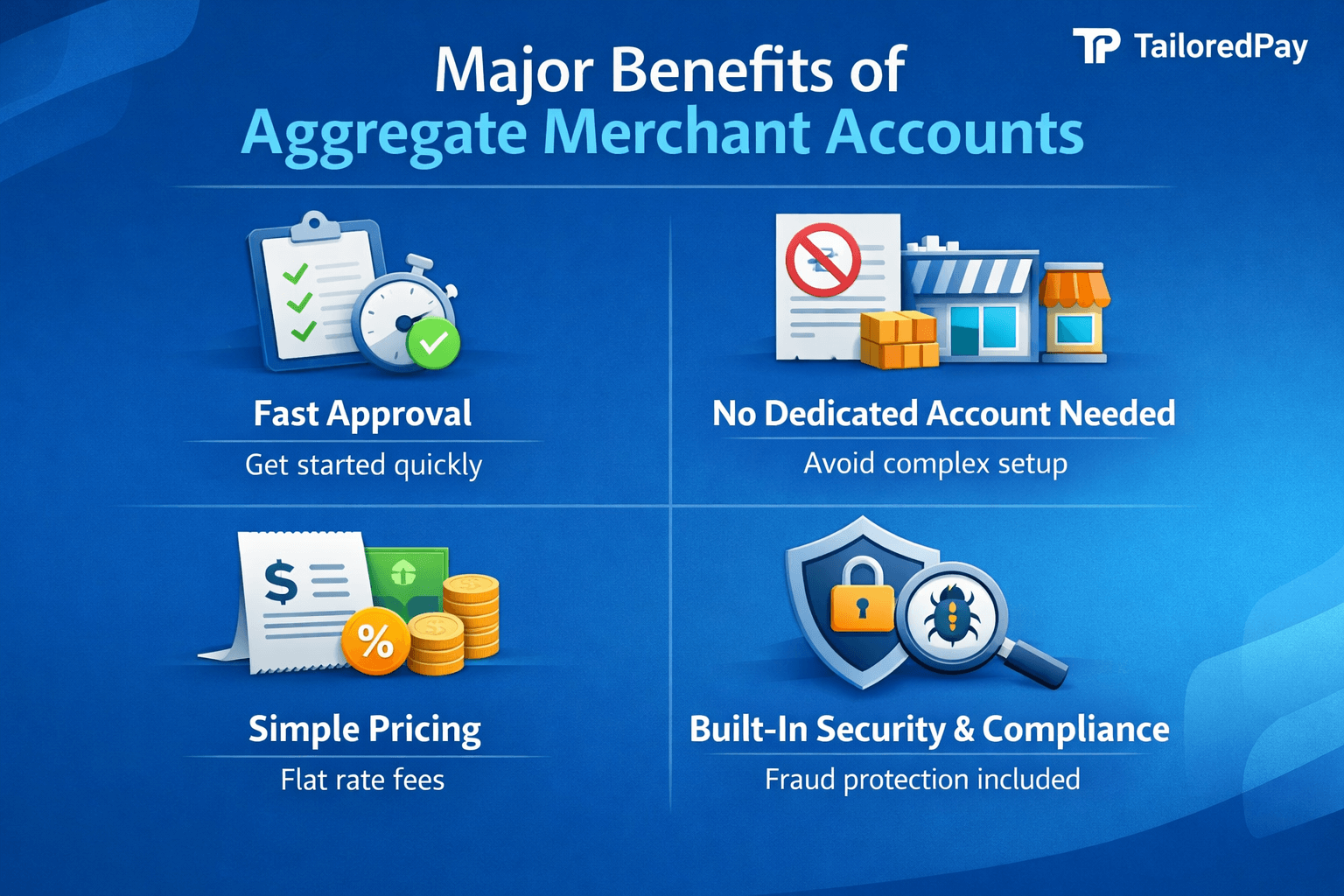

Major benefits of aggregate merchant accounts

Aggregate merchant accounts have become popular for a reason. For many small and low-risk businesses, they offer a fast and simple way to start credit card processing without the complexity of opening your own merchant account.

Here are the main advantages.

Fast approval and easy onboarding

One of the biggest benefits is speed.

A payment aggregator, also known as a payment facilitator, allows you to sign up online and begin accepting payments quickly. There is usually no lengthy underwriting process upfront. Instead of waiting days or weeks for approval, many businesses can start processing the same day.

For startups and new e-commerce stores, this removes a major barrier to entry.

No need to open your own merchant account

With a traditional setup, you must apply for your own merchant account and undergo detailed underwriting. An aggregate model removes that step.

The payment processor handles the master merchant account, and you operate as a sub merchant. This simplifies paperwork, compliance requirements, and bank negotiations, which can be overwhelming for new business owners.

Simple pricing structure

Aggregate providers often use flat rate pricing. You pay a consistent percentage per transaction plus a small fixed amount.

While processing fees may not always be the lowest available, the pricing is easy to understand. Many platforms also avoid long-term contracts, and monthly fees are either low or nonexistent.

For businesses that value predictability and simplicity over customization, this model can be attractive.

Built in compliance and fraud tools

Payment facilitators manage PCI compliance, fraud detection systems, and security standards at the platform level. This reduces the technical burden on individual merchants.

You still need to follow basic compliance rules, but much of the heavy lifting is handled by the provider. For small teams without a dedicated finance or risk department, this is a major advantage.

Ideal for low-risk and small-volume businesses

If you process modest monthly volume and operate in a low-risk industry, an aggregate account can be efficient and cost-effective.

There is less administrative overhead, fewer banking relationships to manage, and minimal setup time. For many small businesses, this tradeoff makes sense compared to the complexity of securing a dedicated merchant account.

That said, while aggregate accounts offer convenience, they are not always the right fit for every business model, especially in higher-risk industries where control and stability are critical.

What to do when you can’t get an aggregate merchant account with a traditional merchant account provider

If you have been declined by a payment aggregator or had your account shut down, you are not alone.

Aggregate providers are built for scale and low-risk merchants. If your business model falls outside their acceptable use policy, for example, CBD, supplements, firearms accessories, travel services, high-ticket coaching, or tech support, your application may be rejected. Even if you are approved, you may face sudden freezes once you start processing higher volumes of online payments.

Here is what you can do next.

1. Understand why you were declined

Before applying elsewhere, identify the real reason behind the rejection.

Common reasons include:

- Operating in a high-risk industry

- High average ticket size

- International sales patterns

- Prior chargebacks or MATCH listing

- Subscription billing with higher dispute risk

Aggregate providers that rely on payment aggregation models protect their master accounts aggressively. If your profile increases risk exposure, they may simply decide you are not a fit.

2. Move from payment aggregation to a dedicated setup

If you cannot get approved under a shared model, the next logical step is applying for a dedicated merchant account.

Unlike a payment facilitator, a traditional merchant account provider performs full underwriting upfront. This includes reviewing your processing history, chargeback ratios, financials, and business model.

While approval takes longer, it creates a more stable structure for processing online payments long-term.

3. Work with a high-risk specialist like TailoredPay

If your business has been declined by mainstream processors, working with a specialist such as TailoredPay can make a significant difference.

TailoredPay focuses on helping high-risk businesses secure a proper payment solution with:

- A dedicated high-risk merchant account under your business name

- A compatible payment gateway for e-commerce and recurring billing

- Risk assessment aligned with your actual industry

- Transparent reserve and fee structures

Instead of relying on payment aggregation, this model gives you your own merchant ID and a direct relationship with an acquiring bank. That separation reduces the chance of sudden freezes caused by pooled risk from other merchants.

For some businesses, TailoredPay can also structure alternative setups that combine card processing with options like bank transfer, where appropriate, helping diversify how you accept payments.

4. Prepare your documentation

High-risk approval requires preparation. Be ready to provide:

- Processing history, if available

- Chargeback reports

- Business registration documents

- Clear product and fulfillment details

- Refund and cancellation policies

A strong application improves your approval odds and can reduce reserve requirements.

The key takeaway

If you cannot get approved by an aggregate provider, it does not mean you cannot accept online payments.

It usually means your business needs a different type of payment solution, one built around proper underwriting rather than broad payment aggregation. For high-risk merchants in particular, a dedicated merchant account through a specialist like TailoredPay is often the more stable and sustainable path.

Get approved for a merchant account in less than 24 hours