2026 Zen Payments Reviews: Pros, Cons, Pricing and More

With about 15 years of industry experience, Zen Payments is one of the most popular merchant service providers specializing in high-risk industries. Zen Payments specializes in working with businesses that traditional providers like Stripe and Square tend to turn down.

Today, we look at Zen Payments’ offer: industries supported, pricing information, reviews from real users and more to help you determine if Zen Payments is the right provider for your business.

Get approved for a merchant account in less than 24 hours

High-risk industries supported

Zen Payments focuses on placing businesses that fall into categories typically flagged as high-risk by traditional processors. Based on available information from their website, partner banks, and user reviews, the provider supports a wide range of industries, including:

- CBD and hemp products: Includes online and retail CBD stores, tinctures, edibles, and related products, provided they comply with local regulations and THC limits.

- Adult and subscription-based businesses: Covers adult content platforms, cam sites, dating services, and other recurring billing models that often face elevated chargeback rates.

- Credit repair and financial services: Businesses offering credit counseling, repair programs, or debt-related services, which are often restricted due to regulatory scrutiny and refund risk.

- Travel and hospitality: Agencies, tour operators, and booking platforms, especially those handling advance payments or large transaction volumes.

- Ecommerce with high chargeback risk: General online stores selling products in categories with historically higher dispute rates, such as supplements, electronics, or dropshipping.

- Subscription and continuity programs: Membership sites, SaaS billing models, and recurring physical product shipments, where billing disputes and cancellations are more common.

- Nutraceuticals and supplements: Vitamins, weight loss products, and wellness supplements, which are often flagged due to marketing claims and refund rates.

- Coaching and online education: Courses, masterminds, and digital programs, particularly those with high-ticket pricing or aggressive marketing funnels.

- Firearms and related accessories: Businesses selling firearms, ammunition, or compliant accessories, depending on acquiring bank policies and jurisdiction.

- Tech support and digital services: Remote tech support, software services, and digital goods, which are sometimes associated with fraud or high dispute levels.

It’s important to note that approval in these categories is not guaranteed.

Zen Payments typically evaluates each merchant based on factors like processing history, chargeback ratios, business model transparency, and compliance with card network rules. Some industries may require offshore merchant accounts or come with stricter terms, such as rolling reserves or capped monthly volumes.

Merchant account services and tailored solutions offered

Zen Payments provides a full range of merchant services tailored to high-risk businesses, going beyond basic payment processing. Based on available information from their website and supporting sources, their core services include:

- High-risk merchant accounts: Dedicated merchant accounts for businesses that are declined by traditional providers, with access to multiple acquiring banks to improve approval chances and long-term account stability.

- Payment gateway integrations: Secure online payment gateways that allow businesses to accept credit and debit cards through ecommerce stores, checkout pages, or payment links.

- Credit card processing (online and in-person): Support for both ecommerce transactions and physical payments via POS systems or card terminals, including chip, swipe, and contactless payments in different currencies.

- Multi-channel payment support: Ability to accept payments across online, mobile, and in-store channels, with flexible setups depending on the business model, credit scores, previous history, etc.

- Same-day or accelerated funding options: Some accounts offer faster access to funds, including same-day funding in certain cases, helping businesses improve cash flow.

- Fraud prevention and chargeback protection tools: Built-in tools such as transaction monitoring, fraud detection, and support for handling disputes and chargebacks, which are critical for high-risk merchants.

- Custom payment solutions and bank matching: Zen Payments works with a network of banks and processors to place merchants in accounts suited to their specific risk profile, volume, and industry requirements.

- Wide payment method acceptance: Support for multiple payment types, allowing businesses to accept different card brands and customer-preferred payment options.

Overall, Zen Payments positions itself as a full-service provider for high-risk businesses, combining merchant account placement, payment infrastructure, and risk management tools into a single offering.

Zen Payments pricing

Zen Payments does not publish fixed pricing on its website. Like most high-risk merchant account providers, it uses a custom pricing model based on your business profile, including your industry, chargeback history, processing volume, and overall risk level.

Custom pricing based on risk

Pricing is tailored to each merchant rather than standardized. Businesses in higher-risk categories such as CBD, adult, or subscription billing, will typically receive higher rates or stricter terms than lower-risk ecommerce businesses. This is standard across the high-risk processing space, where underwriting plays a major role in pricing decisions.

Zen Payments works with a network of acquiring banks, which allows them to match merchants with different pricing structures depending on risk tolerance and approval likelihood.

Interchange-plus pricing model

Zen Payments primarily uses an interchange-plus pricing structure, where you pay the actual interchange fees set by card networks plus a markup from the processor.

This model is generally considered more transparent than flat-rate pricing because it separates:

- Interchange fees paid to issuing banks

- Assessment fees paid to card networks

- Processor markup added by Zen Payments

Your final rate depends on factors like card type, transaction method, and business risk.

Typical transaction fees

While Zen Payments does not publicly list exact rates, third-party sources suggest per-transaction fees starting around $0.30, with a percentage fee applied on top.

Across the high-risk industry, most merchants can expect:

- Around 3.5% to 6.5% per transaction

- Plus a fixed fee per transaction

- Higher rates for card-not-present payments

These ranges vary depending on your approval profile and negotiating power.

Additional and operational fees

Like other merchant account providers, Zen Payments pricing includes several standard fees tied to payment processing. These may include:

- Monthly account or statement fees

- Payment gateway fees for online processing

- Authorization fees for each transaction

- Chargeback fees, typically around $15 to $25 per dispute

There may also be optional costs for hardware, integrations, or advanced fraud tools.

High-risk specific costs

High-risk merchants often face additional requirements that affect pricing. These can include:

- Rolling reserves, where a percentage of funds is held temporarily to offset risk

- Card network registration fees, such as Visa and Mastercard high-risk registration, which can cost around $500 annually

- Volume caps or stricter processing limits

These terms depend heavily on your business model and processing history.

Transparency and setup fees

Zen Payments states that it offers transparent pricing with no hidden fees, and some sources indicate that setup fees may be waived depending on the account.

However, since pricing is not publicly disclosed, merchants need to go through underwriting and request a quote to understand the full cost structure.

Zen Payments pros and cons

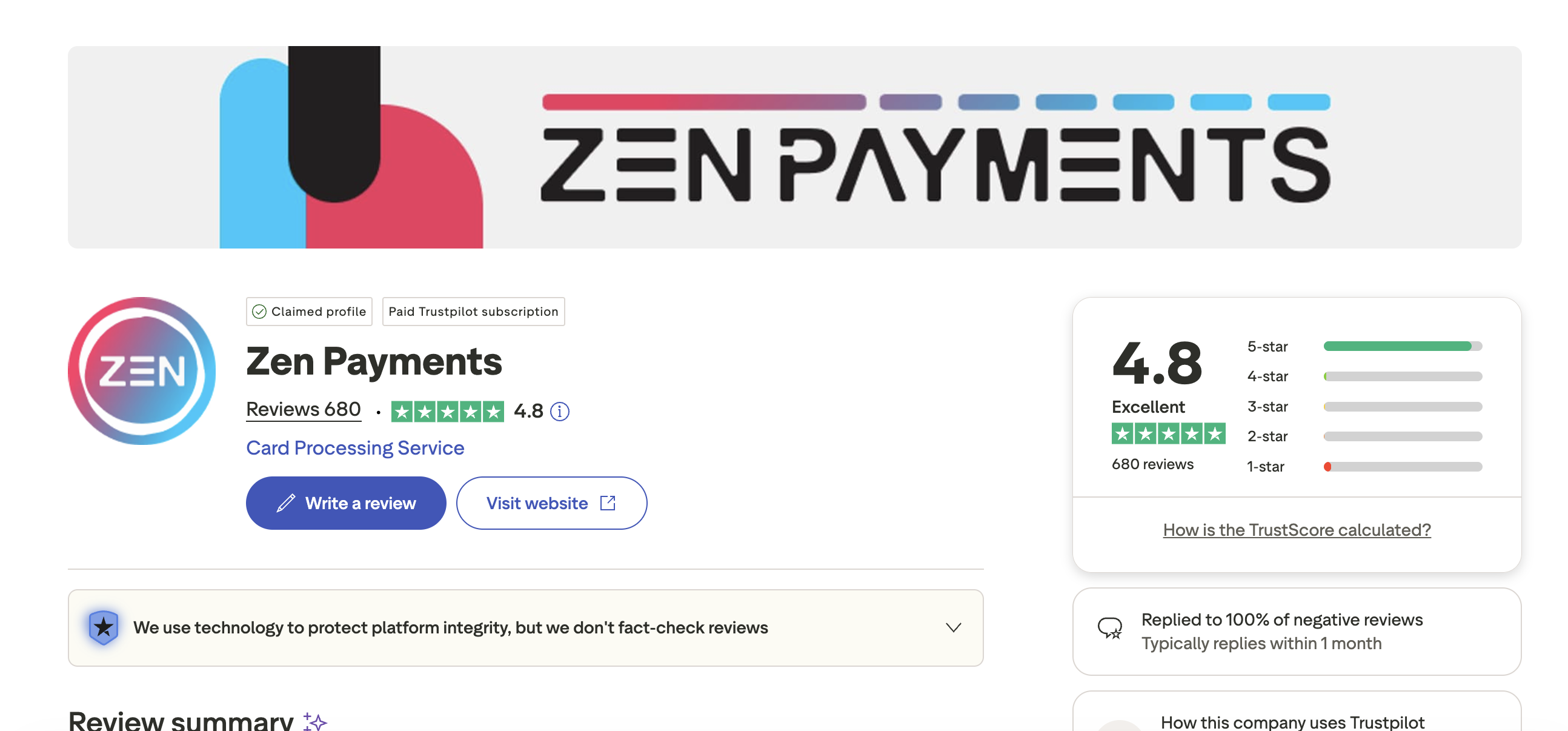

Whether you need to run a few transactions or operate a high-volume merchant account, you should carefully review Zen Payments before getting a merchant account. While there is a ton of positive feedback and many benefits to working with them, all the negative Zen Payments reviews have similar sentiments.

Here’s what you should know, based on real Zen Payments reviews on TrustPilot.

Pro: Zen Payments specializes in working with high-risk businesses

A consistent theme in positive reviews is that Zen Payments helps merchants get approved when other providers decline them, which is critical for high-risk categories.

“I’d been having trouble getting a merchant account approval… they’ve been extremely helpful in getting me approved.” – Source

This reinforces Zen Payments’ role as a placement-focused provider working with multiple acquiring banks.

Pro: Simple and guided onboarding process

Many users describe the onboarding experience as straightforward, with clear communication and step-by-step support.

“The team was professional, responsive, and clear… made everything straightforward.” – Source

For businesses new to merchant accounts, especially in high-risk industries, this reduces friction during setup.

Pro: Strong support during initial setup

Positive reviews frequently highlight individual account reps who stay involved throughout onboarding and early setup.

“Junior called us proactively… made the entire process run smoothly.” – Source

This suggests that support quality is strongest during the sales and onboarding phase.

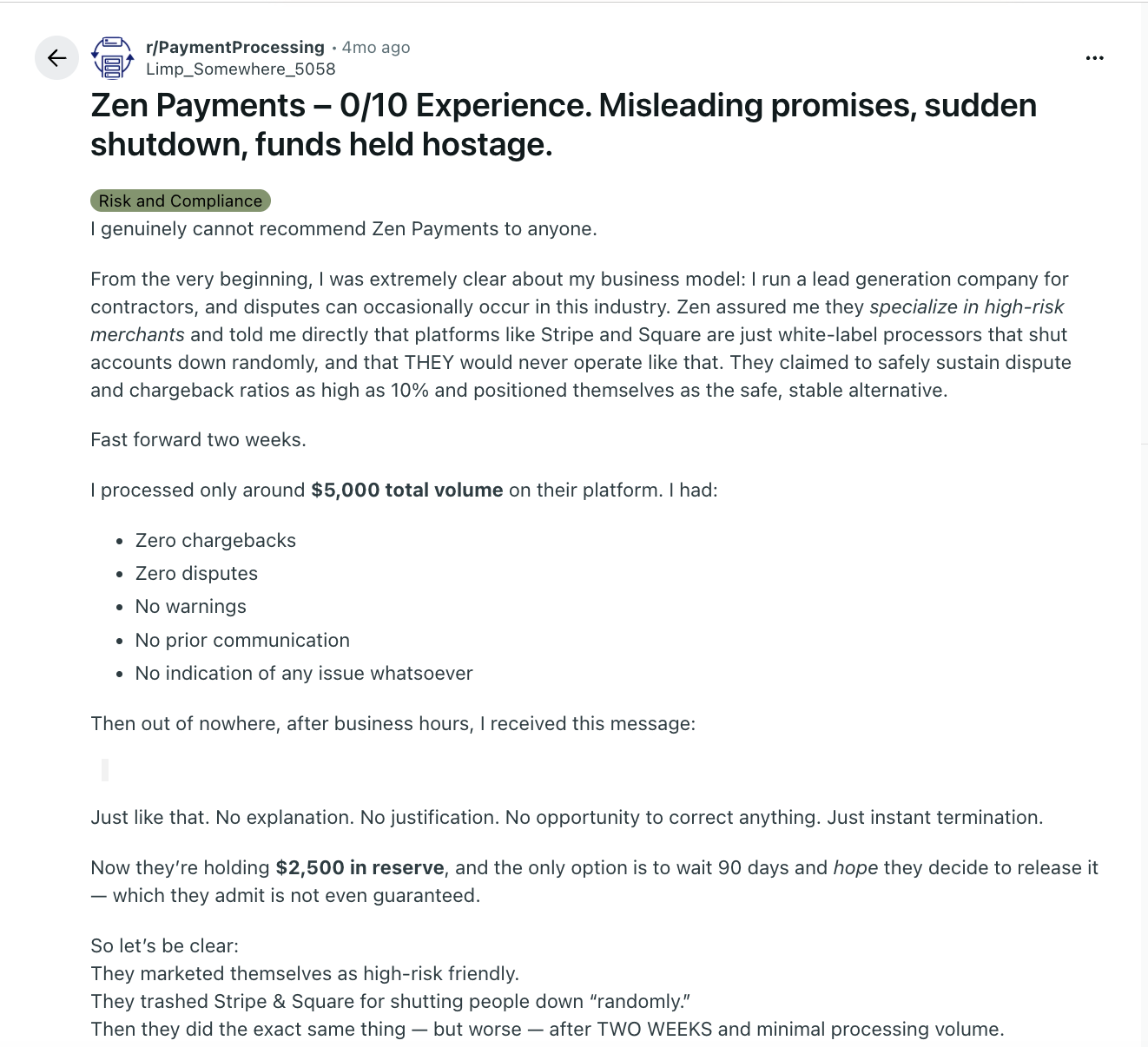

Con: Funds held and reserves applied

A major complaint in 1-star reviews relates to funds being held or reserves applied, sometimes for extended periods.

“Waiting 90 days… holding 10% of all my transactions.” – Source

This is a common issue in high-risk processing, but it can still impact cash flow if not clearly communicated upfront.

Con: Unexpected fees and pricing concerns

Some negative reviews mention higher-than-expected fees or additional charges introduced after onboarding.

“Exorbitant fees (over 10%)… hit with high risk fees with no warning.” – Source

This highlights the importance of reviewing contract terms carefully before signing.

Con: Poor communication and follow-up

Several 1-star reviews point to issues with communication, especially after the account is set up.

“Promised me things… won’t return my call.” – Source

This suggests that while onboarding support can be strong, ongoing communication may vary depending on the case.

There are also cases where Zen Payments approves a high-risk merchant and later turns them down because of a disagreement with the partner bank:

“Just dropped them two weeks ago after almost two years. All was well… until it wasn’t. The bank they were using for my account stopped supporting hemp/d9 thc products and they fumbled hard on the support end. They should have pushed me to another bank in good time, but instead caused my account to get shut down.” – Source

Get a merchant account with TailoredPay instead

Zen Payments can be a solid option for certain high-risk businesses, but reviews show mixed experiences, especially when it comes to reserves, communication, and long-term account stability. If those factors are a concern, it may be worth considering a provider that focuses more heavily on transparency and long-term account management.

TailoredPay works with a wide network of financial institutions, which allows it to match merchants with acquiring banks that fit their exact risk profile, rather than forcing a one-size-fits-all setup. This approach often leads to more predictable terms and fewer surprises after onboarding.

Instead of standard packages for credit card processing, TailoredPay focuses on tailored solutions based on your industry, processing history, and expected volume. This makes it easier to secure terms that actually align with how your business operates, especially if you are dealing with recurring billing or higher chargeback exposure.

Another key difference is how risk is managed. TailoredPay places a strong emphasis on chargeback protection, helping merchants stay below thresholds and avoid account disruptions. This is supported by ongoing guidance and monitoring, not just initial approval.

In terms of user experience, the goal is consistent customer satisfaction across the full lifecycle of the account, not just during onboarding. That includes faster responses, clearer communication, and fewer unexpected changes to terms.

While no high-risk provider is perfect, TailoredPay is built to deliver a setup that works smoothly over time, not just at the point of approval.

Start processing payments in less than 24 hours

Frequently asked questions

Is Zen Payments a legitimate merchant account provider?

Yes, Zen Payments is a legitimate payment processor that has been operating for over a decade. It focuses on high-risk merchant accounts and works with a network of acquiring banks to place businesses that may not qualify with traditional providers.

What types of businesses does Zen Payments approve?

Zen Payments primarily works with high-risk industries such as CBD, adult services, subscription businesses, travel, supplements, and credit repair. Approval depends on factors like chargeback history, business model, and compliance with card network rules.

How much does Zen Payments charge?

Zen Payments does not publish fixed pricing. Costs are custom and based on your risk profile, but most high-risk merchants can expect higher fees than standard processors, along with potential reserves and additional risk-related charges.

Does Zen Payments require a rolling reserve?

In many cases, yes. High-risk merchants may be subject to a rolling reserve, where a percentage of daily transactions is held for a set period. The exact percentage and duration depend on the business and underwriting outcome.

Is Zen Payments a good choice for high-risk businesses?

Zen Payments can be a good option for businesses that struggle to get approved elsewhere. However, reviews suggest that merchants should carefully review terms related to fees, reserves, and payouts before signing, as experiences can vary depending on the account setup.