Merchant Account vs Payment Processor vs Payment Gateway

Are you looking to accept electronic payments for your business? Before a single cent lands on your business’s main bank account, there’s a lot of groundwork to cover first. To accept credit and debit card payments, you need a payment infrastructure in place, which means a merchant account, a payment gateway, and a payment processor.

But what do each of them do, and do you need all three to process payments?

Below, we outline the most important differences between merchant accounts, payment processors and gateways, and what each means for your business. Or, if you don’t have the time, here’s a table summarizing the most important differences and why they matter:

| Merchant account | Payment processor | Payment gateway | |

|---|---|---|---|

| Primary role in the payment process | Temporarily holds funds from credit card payments and debit card transactions | Transmits payment data and obtains authorization | Captures and encrypts card details at checkout |

| Holds funds | Yes, before transferring to your business bank account | No | No |

| Connects to the customer’s account | Indirectly, through the acquiring bank | Yes, communicates with the issuing bank | Yes, captures data entered by the customer |

| Connects to your business bank account | Yes, deposits settled funds into your bank account | No direct connection | No direct connection |

| Handles payment data | Limited, mainly for settlement and risk monitoring | Yes, securely transmits payment data | Yes, encrypts payment data before transmission |

| Underwriting required | Yes, full underwriting by the acquiring bank | Usually limited or bundled | Typically no financial underwriting |

| Main fees involved | Processing rates, monthly fees, chargeback fees, and reserves | Per transaction fees, batch fees | Gateway setup fees, monthly gateway fees, per transaction gateway fees |

| Required for online credit card payments | Yes | Yes | Yes |

Get approved for a merchant account in less than 24 hours

Merchant account vs payment processor: core function in the payment process

A merchant account is a type of bank account that temporarily holds funds from credit card payments and debit card transactions before they are transferred to your business bank account. It sits between your customer’s bank account and your own bank account, acting as a clearing account during settlement.

A payment processor, on the other hand, handles the technical side of the payment process. It securely transmits payment data between the customer’s issuing bank, the card network, and the acquiring bank. It does not usually hold funds itself. Instead, it moves information and authorization requests so the transaction can be approved or declined in real time.

In simple terms, the merchant account stores funds temporarily. The payment processor moves the data that makes the transaction possible.

A payment gateway collects card details at checkout and encrypts that payment data before sending it to the payment processor. In online transactions, the gateway acts as the digital front door of the payment process.

It does not hold funds like a merchant account, and it does not settle payment transactions, but without it, credit card payments and debit card transactions cannot be securely initiated in an e-commerce environment.

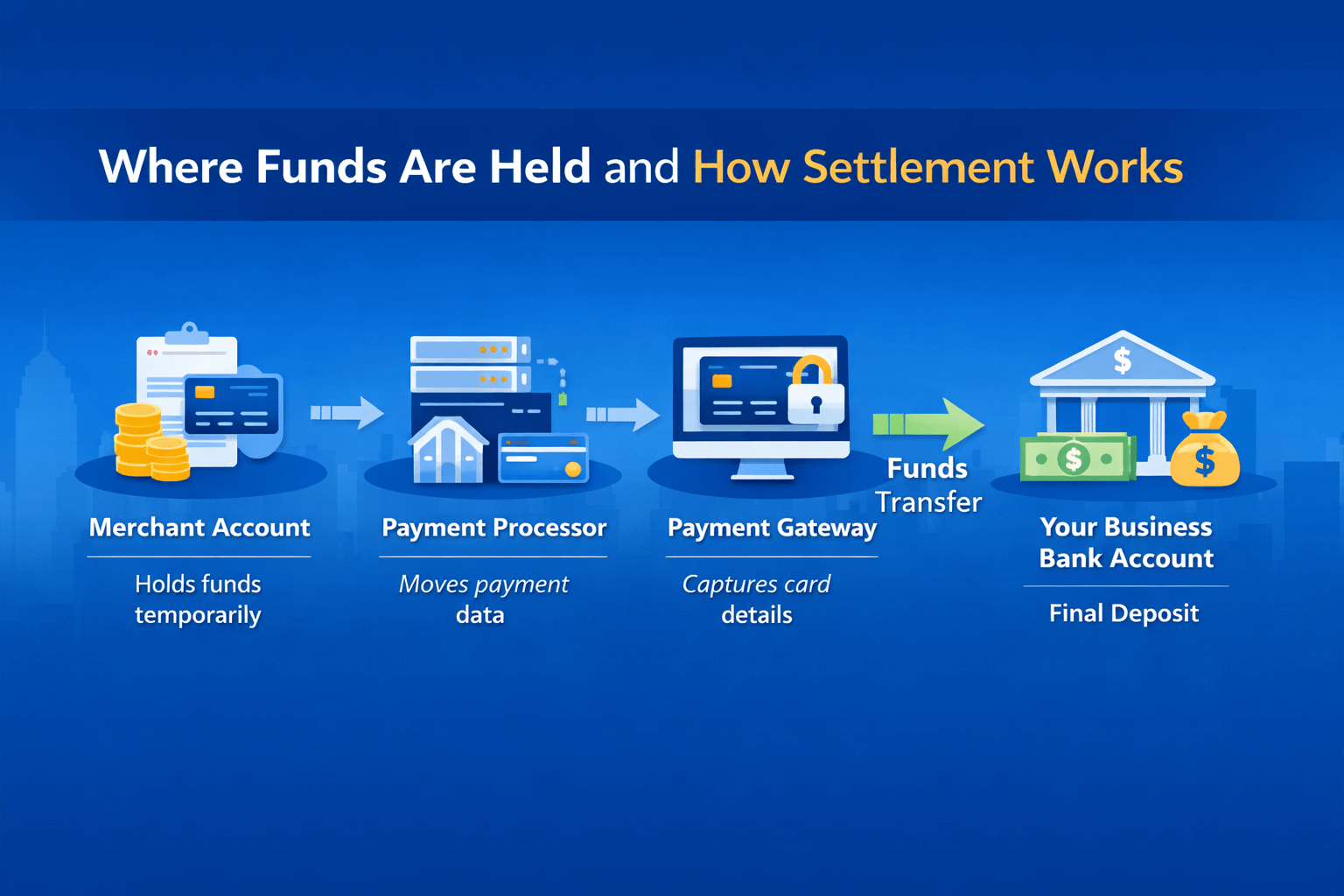

Where funds are held and how settlement works

With a merchant account, approved credit card payments are deposited into a dedicated account under your business name. These funds stay there until settlement is complete, then they are transferred into your business bank account. This is why a merchant account is often described as a specialized bank account for card payments.

A payment processor does not hold funds in the same way. Its role is to transmit payment data and communicate with card networks, banks, and financial institutions. Once a transaction is authorized, the processor triggers the movement of funds, but the actual money flows into the merchant account before reaching your main bank account.

If you want greater visibility into how your debit card transactions are settled, the merchant account is the key component.

A payment gateway also does not hold funds. Instead, it captures the customer’s card details and sends them securely to the payment processor. The gateway never deposits money into your bank account and never stores funds. Its job ends once the payment data is securely transmitted and the authorization request is passed along in the payment process.

Ownership and underwriting requirements

A merchant account is issued by an acquiring bank and requires underwriting. The provider reviews your industry, processing history, chargeback risk, and financial background before approving you. This is especially important for high-risk businesses that may face higher transaction fees or rolling reserves.

A payment processor typically focuses less on underwriting and more on connectivity and infrastructure. Some payment service providers bundle the merchant account and payment processor into one service, which can make it harder to distinguish between the two. Still, from a structural standpoint, they serve different roles within the merchant account and payment processor setup.

If you are applying for a high-risk merchant account, the underwriting process tied to the merchant account will be more detailed than the processor evaluation.

A payment gateway generally does not perform full underwriting on its own. However, gateways may still review your business model to ensure compliance with their acceptable use policies. In most cases, the real financial risk assessment happens at the merchant account level, since that is where funds are held and where exposure to chargebacks directly impacts the acquiring bank.

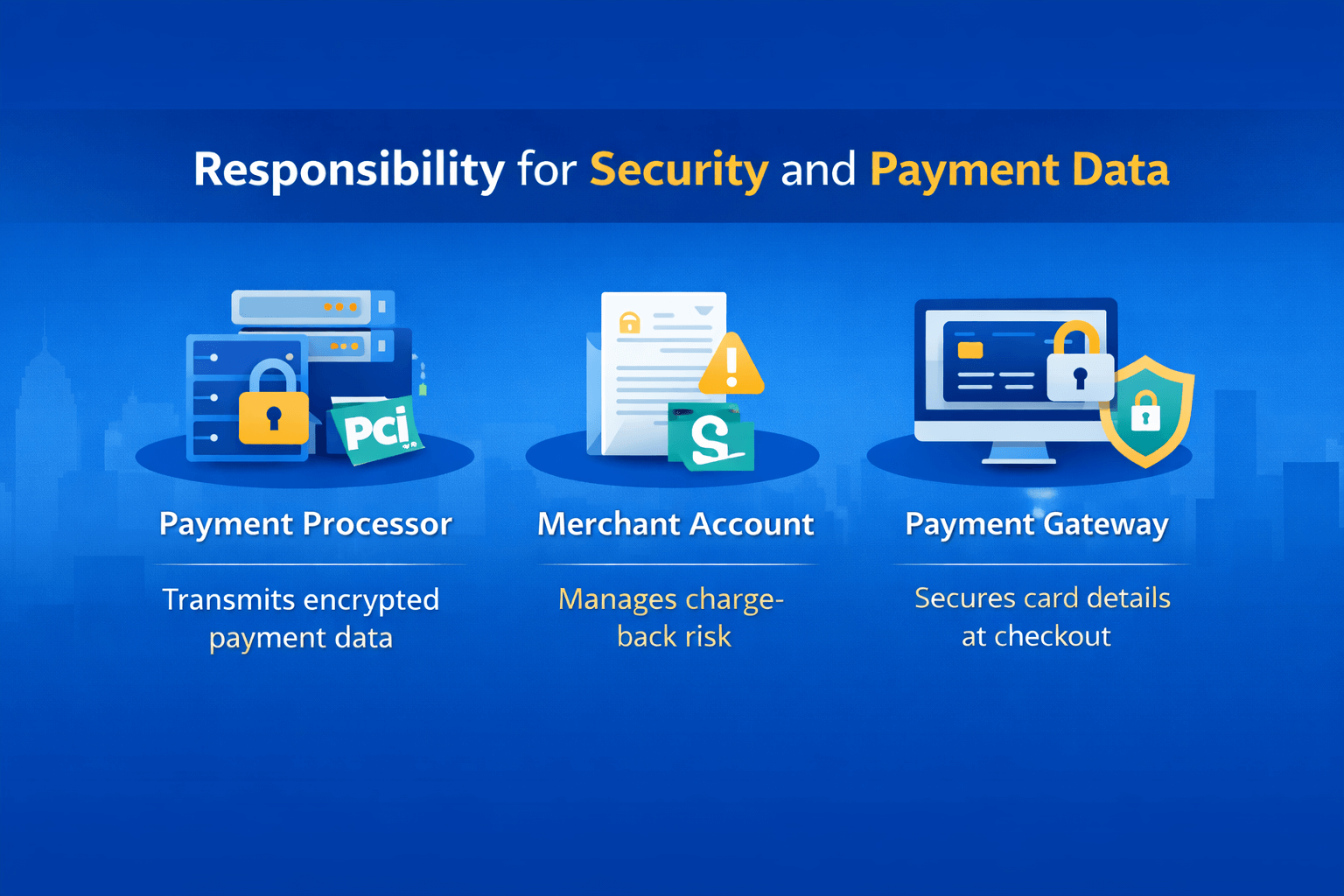

Responsibility for security and payment data

The payment processor is primarily responsible for securely transmitting payment data. It encrypts sensitive card details, communicates with issuing banks, and ensures that customer information is handled according to PCI compliance standards.

The merchant account, by contrast, is responsible for holding funds and managing risk after authorization. It tracks chargebacks, monitors suspicious activity, and may impose transaction fees or reserves if your chargeback ratio increases.

Both are involved in protecting the (online) payment process, but the processor protects the data flow, while the merchant account protects the financial exposure.

The payment gateway focuses on collecting and encrypting card details at the point of entry. When a customer enters the payment information linked to their account, the gateway secures that payment data before it ever reaches the processor. In e-commerce, the gateway is the first security layer, while the processor and merchant account handle transmission and settlement.

Merchant account and payment processor: fee structure and transaction fees

Transaction fees often combine costs from both the merchant account and payment processor, but they are not the same thing.

The merchant account fees may include:

- Processing rates for credit card payments

- Monthly account fees

- Chargeback fees

- Rolling reserve requirements

- The payment processor may charge:

- Per transaction data transmission fees

- Gateway fees

- Batch fees

When merchants review their statements, it can look like a single set of transactions and monthly fees. In reality, you are paying for two distinct services. Understanding how the merchant account and payment processor each contribute to your total cost helps you negotiate better terms and avoid unnecessary expenses.

A payment gateway may also charge its own fees, which can include:

- Setup fees

- Monthly gateway access fees

- Per transaction gateway fees

- Integration or API fees

These costs are separate from merchant account transaction fees and processor fees. When evaluating your total payment process cost, it is important to understand whether gateway fees are bundled or billed separately.

Also, make sure not to fall for promises of completely free merchant accounts, because there is always some fine print involved.

Relationship with your business bank account

A merchant account connects directly to your business bank account, which is where your settled funds are ultimately deposited. Without a merchant account, you cannot directly receive card funds into a traditional bank account.

The payment processor does not replace your bank account or merchant account. It simply facilitates communication between the customer’s account, the card network, and your acquiring bank.

A payment gateway also does not connect directly to your business bank account. The payment gateway serves as a way to connect your website, point of sale system, or checkout page to the payment processor. It never settles funds and never deposits money into your bank account. Its role is limited to initiating and securing the transaction.

In other words:

- Your customer’s account sends the payment request.

- The (online) payment gateway captures and encrypts payment data.

- The payment processor transmits payment data and obtains authorization.

- The merchant account receives and temporarily holds funds.

- Your business bank account receives the final deposit.

Understanding these differences helps merchants choose the right setup, especially when working with high-risk providers that separate merchant account services, payment processing infrastructure, and gateway technology.

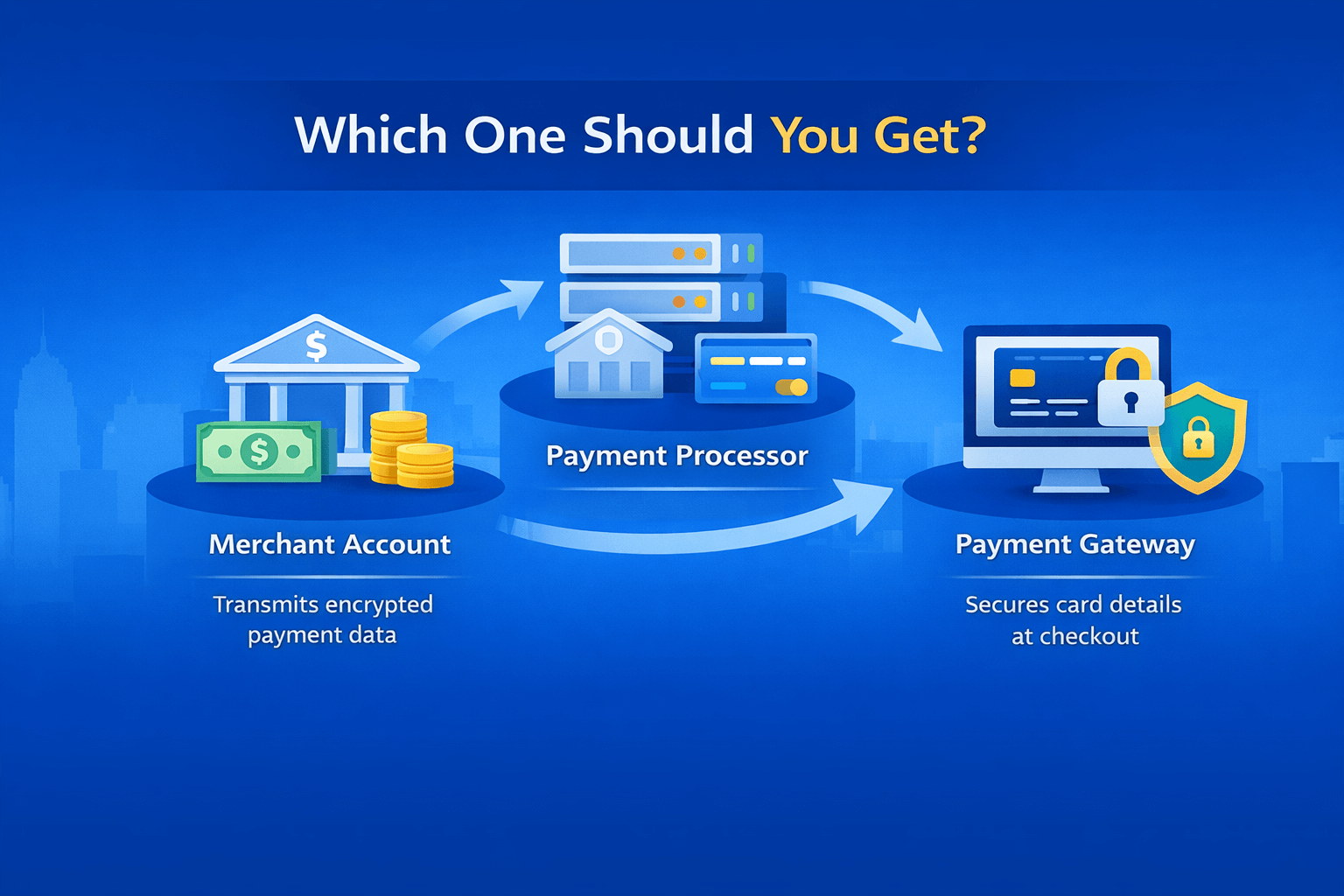

Which one should you get?

The short answer is that you need a merchant account, a payment processor, and a payment gateway if you want to accept credit card payments and debit card transactions, especially online.

They serve different roles in the payment process, so none of them replaces the others.

If your goal is to receive funds into your business bank account, you need a merchant account. This is the account that temporarily holds money after a transaction is approved and before it is transferred to your bank account. Without it, you cannot properly settle card payments from a customer’s account.

If your goal is to securely transmit payment data and get real-time authorization for transactions, you need a payment processor. The processor connects your checkout system to card networks and issuing banks, ensuring that credit card payments are approved, declined, or flagged for review.

If you sell online, you also need a payment gateway. The gateway captures card details at checkout and encrypts that payment data before passing it into the payment process. Without a gateway, you cannot securely collect card information from customers on your website.

In practice, many providers bundle the merchant account, payment processor, and payment gateway into one solution. For low-risk businesses, this bundled setup can be simple and convenient.

However, high-risk merchants often benefit from a specialized merchant account paired with a processor and gateway that understands their industry. This setup can provide:

- More flexible underwriting

- Clearer visibility into transaction fees

- Better chargeback monitoring and fraud detection

- Greater control over reserves and settlement terms

If you are just starting out, the right question is not which one to choose, but which provider offers a strong merchant account, payment processor, and payment gateway combination that fits your risk profile, transaction volume, and industry.

Choosing the right structure ensures your payment process runs smoothly, your payment data stays secure, and your funds move from your customer’s account into your business bank account without unnecessary delays or hidden costs.

Get a high-risk merchant account with TailoredPay

If you operate in a high-risk industry, choosing the right merchant account, payment processor, and payment gateway setup is not optional. It directly affects your approval odds, transaction fees, reserve requirements, and long-term stability.

Many traditional providers focus on low-risk businesses and use one-size-fits-all underwriting models. That often leads to sudden account freezes, withheld funds, or unexpected terminations when chargebacks increase, or risk thresholds are triggered.

TailoredPay works differently.

Instead of forcing high-risk merchants into generic processing models, TailoredPay matches your business with acquiring banks and processing partners that understand your industry. That means clearer expectations around transaction fees, realistic reserve structures, and a payment process built around your actual risk profile.

With the right structure in place, your merchant account is stable, your payment processor handles payment data securely, and your payment gateway supports smooth credit card payments and debit card transactions from your customer’s account to your business bank account.

If you are tired of being declined or restricted by mainstream providers, it may be time to work with a partner that specializes in high-risk approvals from the start.

Get approved for a merchant account in less than 24 hours